As a self-employed individual, you may feel that it will be more difficult to get a mortgage. Perhaps you have already met with your banker and they have refused to grant you the loan for one of the following reasons:

- You haven’t been self-employed for long enough

- You are not declaring enough income

- You have a car loan under your business name and it is blocking you

- Expenses on your tax return have lowered your salary too much

- …

Therefore, when you are self-employed, several reasons can stand in the way of your financial request.

Don’t be discouraged, as a mortgage broker we have access to several lenders with different standards. In some cases, it can even be advantageous to be self-employed. Later, we will see in more detail the advantages of being self-employed when you are looking for a mortgage to purchase a house. For now, I’ll walk you through what you should know before you meet with your banker or mortgage broker.

If you think your net income reported on line 150 of your tax return misrepresents your income, click here. There is a program for you!

Obtain a mortgage loan as a self-employed

The major difference between a self-employed individual and a traditional employee is stability. In fact, an employee with a permanent status will always pretty much earn the same salary. As you must have realized over time, if you are already a self-employed individual, the income is unstable. Some weeks you have no contracts while other weeks it’s madness and the money just keeps coming. Because of this instability, mortgage lenders want more proof of income. Before you can borrow as a self-employed individual you will be asked for two years of income. To determine your eligible income an average of 2 years will be taken. For example, you made $40,000 in 2015 and $45,000 in 2016, the average amount is (40,000 + 45,000) / 2 = $42,500. In the case of a traditional employee, provided they have permanent status at their job, their current salary would be considered to calculate how much they can borrow, that is, $45,000.

If one of the past 2 years does not represent your actual salary, for example, you were injured or you were on parental leave for part of the year, it is possible to select a year that better represents your true income to calculate the average.

Of course, as a self-employed individual, you are eligible to use the Home Buyers’ Plan, a grant or a tax credit for the purchase of a home.

Mortgage: Eligibility criteria for self-employed

- Have held the same job for at least 2 years

- Have 2 years of proof of income

- Have paid all of their previous taxes (proof may be requested)

- Have a credit rating greater than 600 (just like a traditional employee)

- Have a minimum down payment of 5% (just like a traditional employee)

Documents required for self-employed

- You will need to provide the following documents:

- The first 4 pages of your federal income tax return (T1) for the last two years, the statement of income and expenses

- Federal and provincial notice of assessment for the last two years

- If your notice of assessment indicates that you owe a large amount of money, which is often the case with self-employed individuals because they pay taxes at the end of the year. You will need to provide proof of payment

- Proof of the down payment (3 months of bank statements, we must see your name and the logo of your financial institution)

- Promise to purchase accepted and signed by both the buyer and seller

- Property description sheet

The advantage of a mortgage for self-employed individuals

As you know, as a self-employed individual, you can deduct several expenses from your income. Expenses that are related to your occupation. However, some of these expenses are also useful in your day-to-day life. Particularly those that are part of your living expenses such as your car, your cell phone, the internet … Which is a real advantage for your budget as opposed to a traditional employee. Knowing this, banks increase your salary by 15% when calculating how much you can borrow for your home. In the example cited above, you would therefore have an eligible income of 42,500 + 15% = $48,875.

Qualifying income is what allows us to determine how much you may be able to borrow towards the purchase of your home. Thus, with a higher qualifying income, it will be easier for you to get a mortgage or pre-approval.

Obviously, this type of calculation is specific to each bank, therefore not every bank will allow you to increase your salary by 15%. That is why if you have been turned down at your bank or want to improve your chances of obtaining a mortgage, I recommend working with a mortgage broker. He will know which bank to send you to in order to get the best rate and ensure that everything goes well with your file. As luck would have it, I am a mortgage broker and I would be happy to help you buy a house! 😉 438-688-3017

Mortgage for self-employed whose declared income is not an accurate representation

If you thik your declared income is a misrepresentation of your actual income, the good news is there is a program that could help you buy a home.

Mortgage loan for self-employed individuals who self-report their income

The program is called Alt-A and aims to allow self-employed individuals to self-report their income. However, this income must be proven and reasonable. Also, this program requires a 10% down payment on the purchase of the property.

What corporate profile is best suited for this program?

Not all businesses can benefit from the Alt-A program. Here are some criteria that self-employed individuals or businesses must meet:

- It must be a small or medium-sized business.

- Some of the company’s clients must be individuals.

- The company must have several clients.

- It is possible to pay cash.

- There is an income increase year after year.

- The business is making a profit.

- This is a service-based business.

Here are some examples of self-employed individuals and businesses that are well suited for the program:

- IT Specialist, Computer scientist

- Construction: electrician, plumber, carpenter, machine operator …

- Residential services: pruner, exterminator, maintenance worker, lawn care, snow removal …

- Aesthetic services: hairdresser, esthetician, nail technician …

- Health services: chiropractor, osteopath, massage therapist, personal trainer …

- Various services: tattoo artist, mechanic, building inspector …

Alt-A mortgage: eligibility criteria for self-employed who self-report their income

- The company must have been in existence for at least 2 years

- You must have 2 years of proof of income

- You must present self-reported income that makes sense in relation to the sector of activity

- You must have paid in full all previous taxes (proof WILL BE required)

- A very good credit history is required

- you must have a 10% minimum down payment

- You must purchase a building with a maximum of 2 units (duplex), one unit of which must be occupied by the borrower.

- Maximum value of the building is $1,000,000.

- The maximum loan amount is $600,000

Additional program fees for self-employed individuals who self-report their income

Not all lenders adhere to the Alt-A program. It is also possible that the interest rate will be slightly higher when using this program, anywhere from 0.05% to 0.2% more.

Mortgage insurer: Sagen or Canada Guarantee

The Alt-A program is offered by Sagen (formely known as Genworth) and Canada Guaranty, both are mortgage insurers. You are probably familiar with the Canada Mortgage and Housing Corporation (CMHC); Sagen and Canada Guranty offers the same types of services.

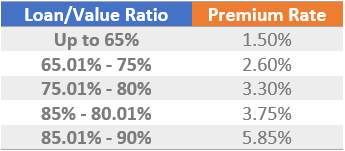

Mortgage insurance fees for the Alt-A program are higher than for a purchase where the income is not self-reported. Here is a comparison of both situations:

Mortgage WITHOUT the Alt-A self-reported income program (10% down payment)

Loan = $300,000

Sagen cost (3.1% * of $300,000) = $9,300

Sagen premium tax, payable directly to the notary (9% of $9,300) = $837

Loan + premium (3.1%) = $309,300

Monthly payment at 3% = $1,463.75

Mortgage loan WITH the Alt-A self-reported income program (10% down payment)

Loan = $300,000

Sagen cost (5.85% * of $300,000) = $17,550

Sagen premium tax, payable directly to the notary (9% of $17,550) = $1,579.50

Loan + Sagen (5.85%) = $317,550

Monthly payment at 3% = $1,502.79

A difference of about $39 / month ($1,503- $1,464 = $39).

* Premiums may vary. They were updated on November 03 2020.

As you can see, there is a price difference. We therefore only use this program when necessary. However, it is very convenient for some clients as it allows them to buy a house!

If you have any questions about this, please feel free to post them in the comments, send me an email at bruno.gag.st@gmail.com, or call me at 438-688-3017.

Sources